Some days you wake up and realize the system is designed to keep you paying, even when you’re trying to escape the system. Like when you finally summon the courage to wipe out $90k in debt, only to get a bill for $30.10 in the mail for the privilege. That’s right — you have to pay to prove you have no money.

This isn’t just some abstract complaint. It’s the reality hidden in the fine print of financial recovery. Let’s trace the clues.

The Evidence

PACER’s Sneaky Waiver

You think you’re being smart, avoiding those $0.10-per-page charges on PACER. But wait — if your tab runs under $30 a quarter, the bill vanishes. It’s like finding a loophole in the loophole. Except sometimes you get that $30.10 bill anyway. The system knows exactly how much to charge to make you feel stupid.

Who knew government databases had such a dark sense of humor?The $90k Debt That Vanished (Almost)

At 26, buried under medical bills and unemployment, one person filed Chapter 7 and walked away from $90k in debt. The cost? $1,700. That’s less than 2% of what they wiped out. It should be a victory story. Instead, it’s just another data point in how broken the system is.

How do you even accumulate $90k by 26? The answer isn’t what you think.

The Credit Score Paradox

That $30 PACER bill suddenly feels like the least of your problems.

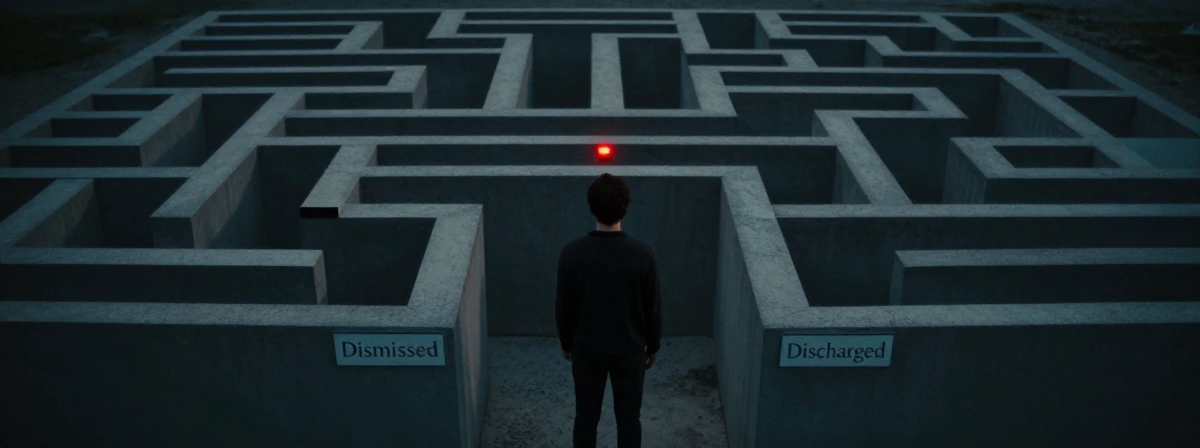

You’re in debt up to your eyeballs. The logical move? Declare bankruptcy and start fresh. But then you remember: your credit score is used for everything from apartments to jobs. It’s not just about new debt — it’s about basic survival.Dismissed vs. Discharged — The Fine Print That Kills

There’s a reason 90% of bankruptcy cases are dismissed. Miss a payment, miss a form, miss a meeting — and poof. You’re back where you started, now with a bankruptcy mark on your record and all your original debts intact. It’s like a game where the rules change every minute.

The real question: why do they make it so easy to fail?

The Bankruptcy Nerd’s Secret

Some people game the system. They file Chapter 13, let creditors miss deadlines, and walk away with half their debt wiped out. It’s not “ethical” by any stretch, but it works. The system has so many moving parts, someone’s bound to find a weak link.

Maybe that $30 PACER bill is just the price of admission to the real game.Student Loans: The Undischargeable Nightmare

You can wipe out credit cards, medical bills, even car loans. But student loans? Good luck. The system that supposedly helps you when you can’t pay expects you to keep paying the loans that put you in this mess. It’s like being told to swim upstream while someone keeps pushing you back.

No wonder people stay in debt forever.

The Verdict

The $30 bill isn’t just about money. It’s about the whole system’s subtle cruelty. They make you pay to access court records, pay to file for relief, pay to rebuild what you lost. It’s not about fairness — it’s about control.

Next time you see a $0.10 charge on your PACER bill, remember: you’re not just paying for a document. You’re paying to participate in a game designed to keep you playing forever. And maybe, just maybe, that’s the real debt you can never discharge.